Fetching Historical Yield Curves from B3

Source:vignettes/Fetching-historical-yield-curve.Rmd

Fetching-historical-yield-curve.RmdData for the yield curve is available in B3’s website. The data is built using interest rate futures. See this pdf for more details about the source of the yield curves.

library(rb3)

#> rb3: 35 templates registered

library(ggplot2)

library(stringr)

library(dplyr)

#>

#> Attaching package: 'dplyr'

#> The following objects are masked from 'package:stats':

#>

#> filter, lag

#> The following objects are masked from 'package:base':

#>

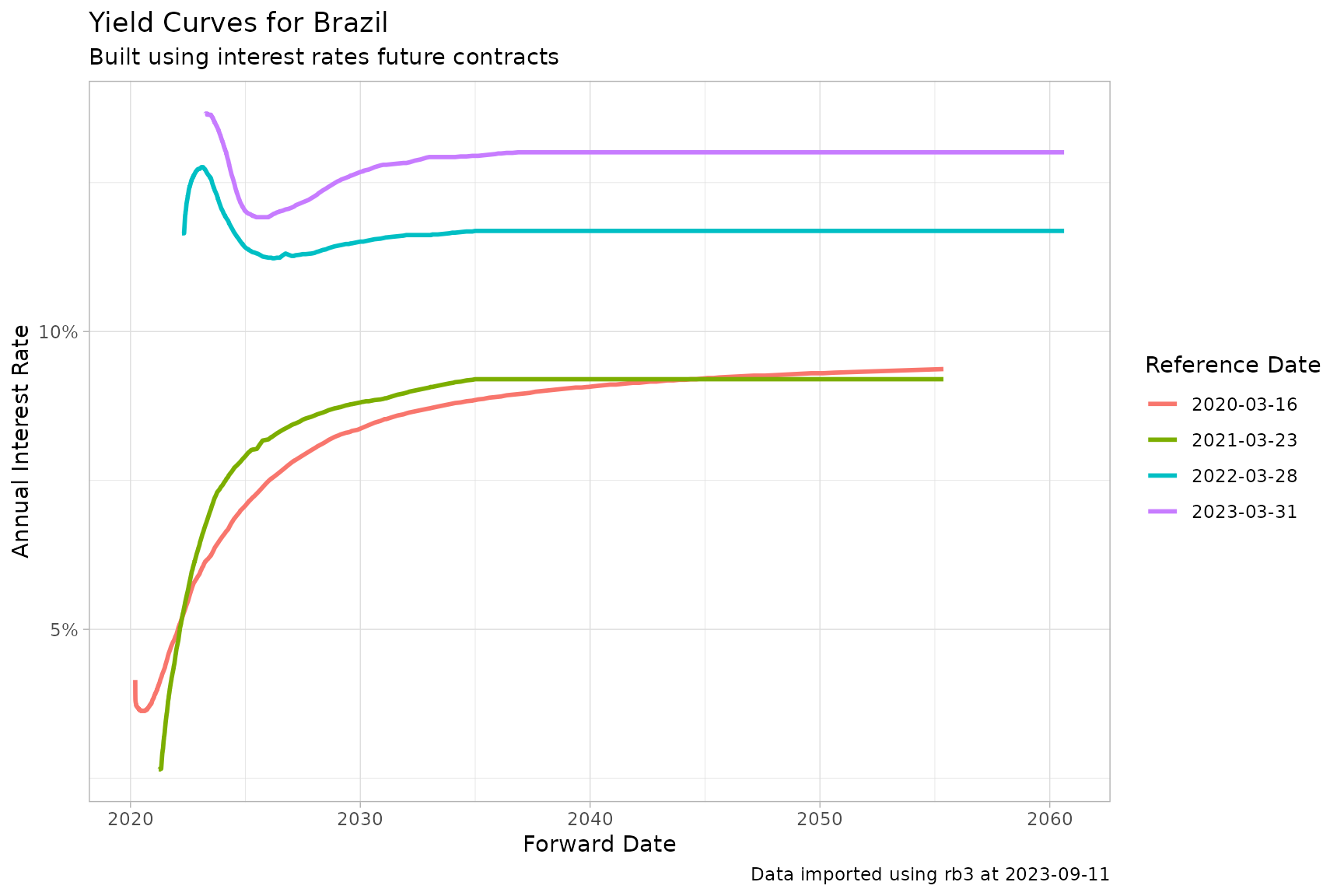

#> intersect, setdiff, setequal, unionDI X Pre Curve

p <- ggplot(

df_yc,

aes(

x = forward_date,

y = r_252,

group = refdate,

color = factor(refdate)

)

) +

geom_line(linewidth = 1) +

labs(

title = "Yield Curves for Brazil",

subtitle = "Built using interest rates future contracts",

caption = str_glue("Data imported using rb3 at {Sys.Date()}"),

x = "Forward Date",

y = "Annual Interest Rate",

color = "Reference Date"

) +

theme_light() +

scale_y_continuous(labels = scales::percent)

print(p)

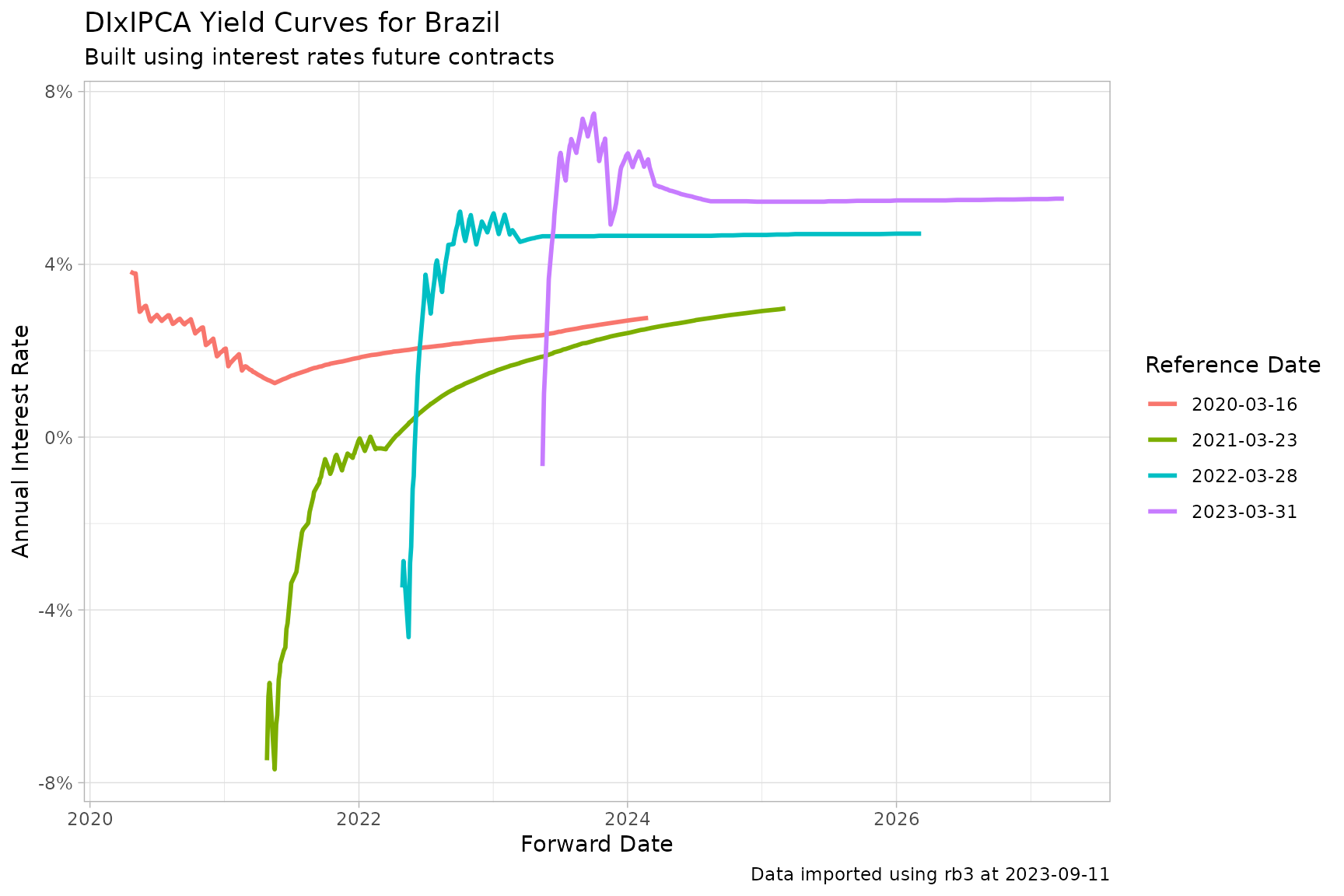

DI x IPCA Curve

df_yc <- yc_ipca_mget(

first_date = Sys.Date() - 255 * 5,

last_date = Sys.Date(),

by = 255

)p <- ggplot(

df_yc |> filter(biz_days > 21, biz_days < 1008),

aes(

x = forward_date,

y = r_252,

group = refdate,

color = factor(refdate)

)

) +

geom_line(linewidth = 1) +

labs(

title = "DIxIPCA Yield Curves for Brazil",

subtitle = "Built using interest rates future contracts",

caption = str_glue("Data imported using rb3 at {Sys.Date()}"),

x = "Forward Date",

y = "Annual Interest Rate",

color = "Reference Date"

) +

theme_light() +

scale_y_continuous(labels = scales::percent)

print(p)

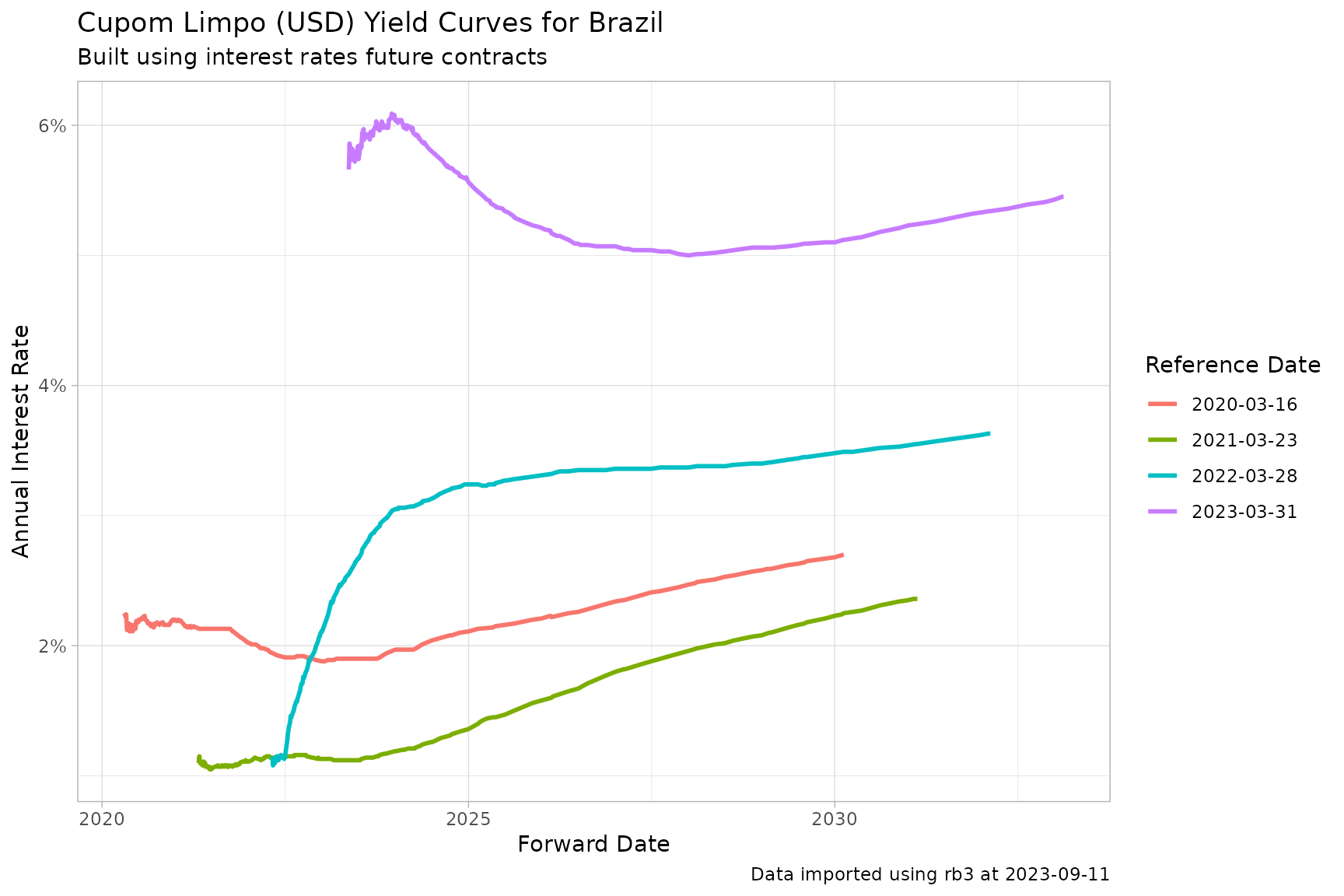

Cupom Limpo (USD)

df_yc <- yc_usd_mget(

first_date = Sys.Date() - 255 * 5,

last_date = Sys.Date(),

by = 255

)p <- ggplot(

df_yc |> filter(biz_days > 21, biz_days < 2520),

aes(

x = forward_date,

y = r_360,

group = refdate,

color = factor(refdate)

)

) +

geom_line(linewidth = 1) +

labs(

title = "Cupom Limpo (USD) Yield Curves for Brazil",

subtitle = "Built using interest rates future contracts",

caption = str_glue("Data imported using rb3 at {Sys.Date()}"),

x = "Forward Date",

y = "Annual Interest Rate",

color = "Reference Date"

) +

theme_light() +

scale_y_continuous(labels = scales::percent)

print(p)